– Platforms net cashflows were $750 million, up 76% on Q3 23

– North inflows from Independent Financial Advisers (IFAs) increased 47% on Q3 23 to $832 million

– Platforms Assets Under Management (AUM) increased to $78.1 billion (Q2 24: $74.7 billion)

– Superannuation & Investments AUM increased to $55.8 billion (Q2 24: $54.0 billion), with net cash outflows reducing 46% to $334 million (Q3 23: net cash outflows of $619 million, excluding $4.3 billion mandate loss)

– New Zealand Wealth Management net cashflows were $40 million (Q3 23: $6 million), and AUM increased to $11.6 billion (Q2 24: $11.2 billion)

– AMP Bank total loan book of $23.0 billion, from $22.9 billion in Q2 24

– AMP Bank total deposits of $20.9 billion, from $20.6 billion in Q2 24

AMP Chief Executive Alexis George said:

“During the quarter, AUM increased across Platforms, Superannuation & Investments and New Zealand, and net cashflows also improved across these businesses. Platforms cashflows significantly increased on the prior period, while in Superannuation & Investments, outflows were almost halved, with a continued focus on our renewed member proposition and a new national advertising campaign for AMP Super.

“Our Platforms retirement solution, MyNorth Lifetime, is attracting interest from aligned and independent advisers, and was recognised as a finalist at the AFR BOSS Most Innovative Companies 2024 Awards earlier this month.

“The launch of our small business and consumer digital bank remains on track, with a first release to AMP employees in the coming weeks, ahead of a public launch in Q1 25, with marketing of the new proposition underway. While we progress towards launch of this new bank division, in our existing bank we continue to carefully manage margins through restrained loan growth, given the competitive funding environment.

“The new partnership for our Advice business is on track, with completion of the transaction to occur before the end of the year. Our focus remains on a smooth transition and maintaining the strong relationships with advisers as they move to the new joint venture with Entireti.

“Last week we completed the return of $1.1 billion of capital to shareholders, via on-market share buybacks and the recommencement of dividends. This is an important milestone in the transformation of AMP, as we continue to simplify and grow the business.

Business unit results

Platforms

Net cashflows (excluding pension payments) were $750 million for the quarter, up 76% (Q3 23: $426 million). Flows into AMP’s North platform from independent financial advisers (IFAs) increased by 47% on Q3 23 to reach 36% of total inflows. Pension payments were $516 million (Q3 23: $499 million).

AUM increased to $78.1 billion (Q2 24: $74.7 billion), supported by positive investment markets. North’s managed portfolios offer continues to grow, increasing 12.3% to $17.9 billion at the end of the quarter (Q2 24: $15.9 billion).

Superannuation & Investments (formerly Master Trust)

Superannuation & Investments net cashflows (excluding pension payments) improved to an outflow of $334 million, from $619 million in Q3 23 (excluding the $4.3 billion mandate loss in Q3 23). This reflects resilient inflows and improved outflows, driven by the renewed focus on the member proposition. Pension payments were $101 million (Q3 23: $106 million).

AUM increased to $55.8 billion (Q2 24: $54 billion), reflecting positive investment markets, partially offset by the net cash outflows and pension payments.

New Zealand Wealth Management

New Zealand Wealth Management Net cashflows were $40 million (Q3 23: $6 million), driven by lower outflows as a result of the sale of legacy products after Q3 23. Pension paymentsaa were broadly steady at $41 million (Q3 23: $42 million).

AUM increased slightly to $11.6 billion (Q2 24: $11.2 billion), with positive investment markets driving returns.

AMP Bank

AMP Bank’s total loan book was $23.0 billion (Q2 24: $22.9 billion), with the residential mortgage book stable given AMP’s strategy to manage margins in the highly competitive environment. Credit quality remains strong, with 90+ days arrears remaining low at 0.89%.

Total deposits were broadly steady at $20.9 billion (Q2 24: $20.6 billion), with inflows largely from at call deposits.

The small business and consumer digital bank remains on track to launch in Q1 25, to help diversify revenue and funding mix.

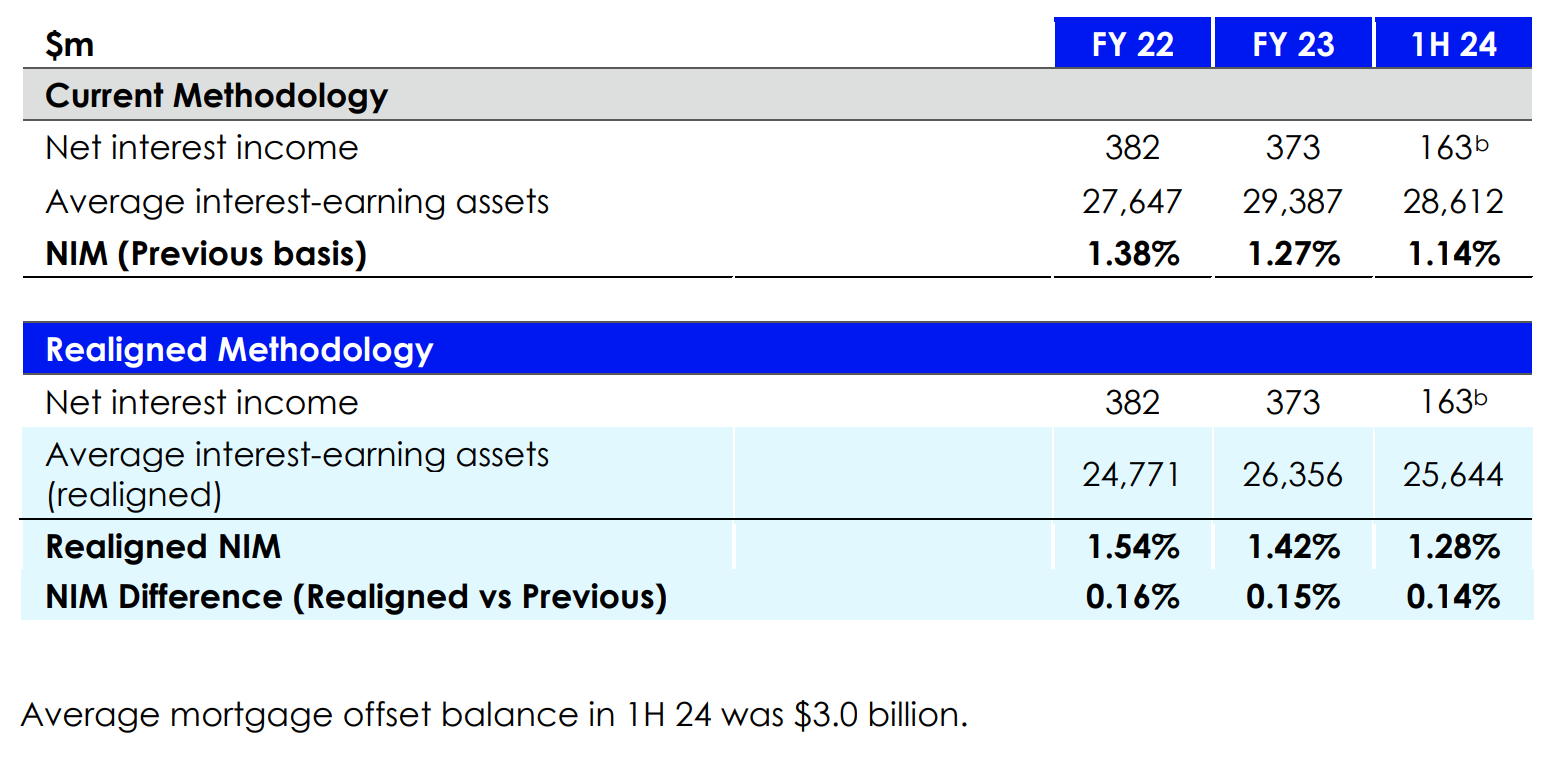

NIM methodology

Net Interest Margin is being restated to align the treatment of mortgage offset accounts with industry practice. Under the new methodology, the value of offset accounts will be deducted from the Interest-Earning Assets balance. This new NIM methodology will be used going forward.

FY 24 NIM guidance remains unchanged, adjusted for this new methodology. FY 24 NIM is expected to be between 1.24% and 1.29% (previously stated 1.10% - 1.15%)

a. Pension payments for NZWM has been defined as “Partial Withdrawals from superannuation products made by members over the age of 65”. A Partial Withdrawal is defined as a withdrawal made from an account which is not subsequently closed.

b. Half year figures have been annualised

All amounts are in Australian dollars (A$) unless otherwise stated. Authorised for release by the Market Disclosure Committee.